Rolling, Bad Accounting, and Double Hockey Sticks Graph

Portfolio overwriting is not a silver bullet, and you can easily lose money if you don’t know what you are doing.

Full Stop.

Repeat: you can lose money.

I don’t think that the options education out there sufficiently emphasizes and explains how. Aside from upside risk and downside risk, there are other, less straightforward ways to lose money. Oddly enough, most of them manifest when you are trying to actively manage your positions. . . so much so I want to point out, before I go into the specifics, that rolling and BTC (Buying to Close) in a way that causes a loss always occurs when you “buy into” positions.

I may never reach a conclusion on that philosophical dilemma. But in the meantime, we will explicitly cover the ways to make your account shrink with bad covered call trading. I want to point out, before I go into the specifics, that rolling (unless it generates enough premium to cover the cost-to-close) will always cause an initial loss because you “buy into” positions. Theta and appreciation may offset and eventually overtake that loss over time, but any time you pay into

a position, it is in a way a “loss” if, after accounting for premiums received, it decreases your cash balance below where it was when you sold the initial call.

Rolling Risks

Firstly, let’s criticize rolling down. Rolling down can easily lock you into a loss. So easily, in fact, that I never roll down my index covered calls to a strike below cost basis. Whatever premium you received should have been enough when you set the trade up.

Further, even if the price of the underlying asset falls and you have to wait months for your shares to come back to their cost basis, you should be able to flex those passive FIRE investor muscles in the interim. Unless you are actively monitoring, adjusting, and rolling up and/or out constantly before price appreciation overtakes your strike; then you will find yourself in the money, and at a loss (that was a very intentional double entendre).

Rolling up has a different risk: you are paying into your position and raising your cost basis. Compare this to the idea of lowering your cost basis over time with call premiums – it’s the exact opposite! Like I said, in general, we don’t want to pay into our trades in the portfolio overwriting world. For other strategies, there are perfect times to adjust positions and pay into options, but for the purposes of FIRE overwriting I don’t think it’s a good habit to get into. You are gambling more money, hoping that you retain whatever appreciation made you roll up in the first place, and a simple drop in the security price can make whatever you paid into the position quickly evaporate.

Rolling out or up and out tends to keep you from paying cash from your account into your positions (but always realize you are still “paying” with the time value and original premium when you BTC and roll). This is generally better than rolling up alone. But you can only roll up and out so many times before you run out of months to roll to, and you eventually end up ITM. As a general rule, for the explicit goal of monthly income generation via portfolio overwriting, rolling out past a 90 DTE (expiration) usually isn’t worth your time (literally).

Another problem is that the risk of loss for these adjustments shifts into the “lost profits” category. Why? Because of time value inequity, the farther into the future you go, the less call premium per time you get.

Time Value Inequality

This idea behind time value inequality is readily apparent if you take the premium for a call and divide it by the number of days until expiry, and then compare it to a longer-dated call. That premium per day will decrease substantially for longer dated calls. Ergo, when we roll out or up and out, the total premium we receive will be less per day than the call you initially sold. And remember, it is the initial premium received plus the amount received when you rolled, not the total value of the new sold call; you will have technically “paid into” the new position with the initial premium received when you roll. You will need to recalculate expected ROI and decide if you are ok with the lower number.

Clerical Errors

Bad accounting can also be a risk when you are deciding whether to BTC positions early. There are multiple examples in prior chapters, but we will rehash it again here in case you aren’t reading sequentially or would like a refresher. After a roll, your new sold call’s value in your account is not equal to the amount of premiums you received in your account, if you are considering it to be a continuation of the same position you had when you sold the first call. You “paid into it” when you rolled, and therefore closing it early may actually cause you to spend more closing something than you made from theta decay.

From the earlier chapter: If you sell a call for $1.25, but it becomes in the money and appreciates to $3.00 (a $1.75 loss to you), then roll to a $3.95 contract at a later date, you would have only received $1.25 plus $0.95.(( In fact, the roll itself would only show a +95 transaction when you placed the combination trade as a single order to BTC one call and sell to open another, because you pay $300 to close and receive $395, netting you $95. )) So, receiving $2.20 in premiums is good, but if you close out that $3.95 position at any point before theta decay pares it down to $2.20, you are losing money.

Losing Money By Biding Time

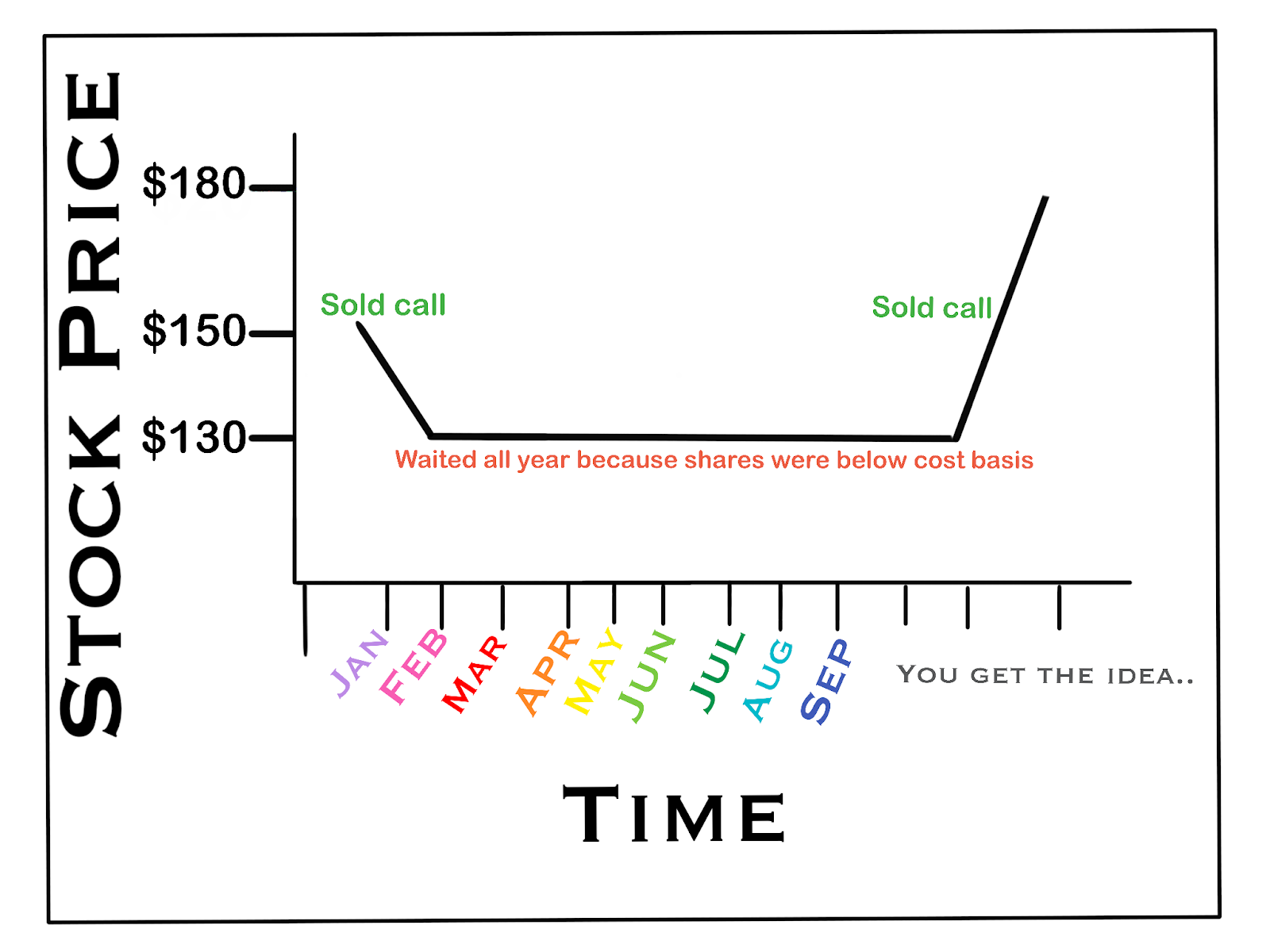

Finally, we need to dip into path-dependence, which is a consideration of how the order of events (price moves) affects investment returns. Consider the following time series. You buy VTI at $150 in January and sell a call. It drops to $130 and stays there all year. Meanwhile, you wait patiently for the share price to come back to your cost basis of $150. Then, in December, it starts to rise. When it hits $150 you get excited and sell a call again, capping your profits. It keeps going up and ends at $180 for the year.

So, VTI did well for the year— it made 20%. You, as the call seller, didn’t hit that mark, and only made two call premiums. This illustrates a lot of things to consider about how stocks make money, especially when considering when exactly to buy and sell. The first takeaway is that the first month when the index dropped, portfolio overwriting was a win. Secondly, if your cost basis was low enough that a $130 call was still OTM,1 you could still have been selling calls and making premiums all year.

Third, buy and hold wins just from the one major move at the end of the year.2 We saw an idealized example of this followed by an immediate dose of reality in the chapter on overwriting and returns. Because you don’t know how the market will move, but as a Boglehead you do expect it to trend up, portfolio overwriting all your shares of something you have a long-term bullish outlook on would be counterintuitive.

By extension, we also know that indexes pull back often, either as part of normal variance or due to the occasional financial crisis. Allocating a portion of your portfolio to covered calls will basically

diversify your investments into an asset that outperforms ordinary shares on those pullbacks. So there is some serious logical financial justification3 to be found beyond just income generation when it comes to portfolio overwriting (if you are looking for it).

Although this drastic move isn’t the most common behavior for the total market, the concept is the key. But as you will see in the next chapter, we can try to minimize loss from these situations. I also introduce one more way you can get stuck trading covered calls.

Next: Article 32– Martingales and Ladders

Previous: Article 30– Position Management– Rising Price– Rolling Up and Out

- One nice thing I’ve noticed about portfolio overwriting for FIRE is that due to continuous dollar-cost averaging, most of the time your cost basis will be below

market value. [↩] - This is because the long shares are long volatility and delta positive, whereas a short call is the exact opposite. Selling the short call pays us to give up that one big, potential win in exchange for the smaller, certain return. [↩]

- 4And just as many counter-arguments. [↩]