Plus More on Calculating Expected Returns

So you own 100 shares, you’re going to sell a call— but which call to sell? Not an easy answer, but you should always start with this question— how much are you expecting to make? It’s time to look at returns, and all the fun stuff you can do with those numbers.

Example Portfolio Overwriting Returns

We’ll use VTI for these calculations, with a chain taken on 12/13/29 when the share price was $161.27

Say you are (like most Mustachians) a diligent Boglehead, and have worked hard to accumulate 100 shares of VTI. Looking at your account there’s $16,127 worth of VTI sitting there growing like a gorgeous lophophora williamsii button.

You know to weather the storm, sit tight, and over time the market is going to go up, and up, and up. But for whatever the reason you want extra cash, and don’t want to sell your shares.

Conundrum? Not really. Taking a look at the chain, you see that the $162 strike price call has a bid-ask of $1.35-$1.50

So you’ll probably get $140 ($1.40 a share) for selling someone the right to buy 100 shares of VTI from you for $162 a share.

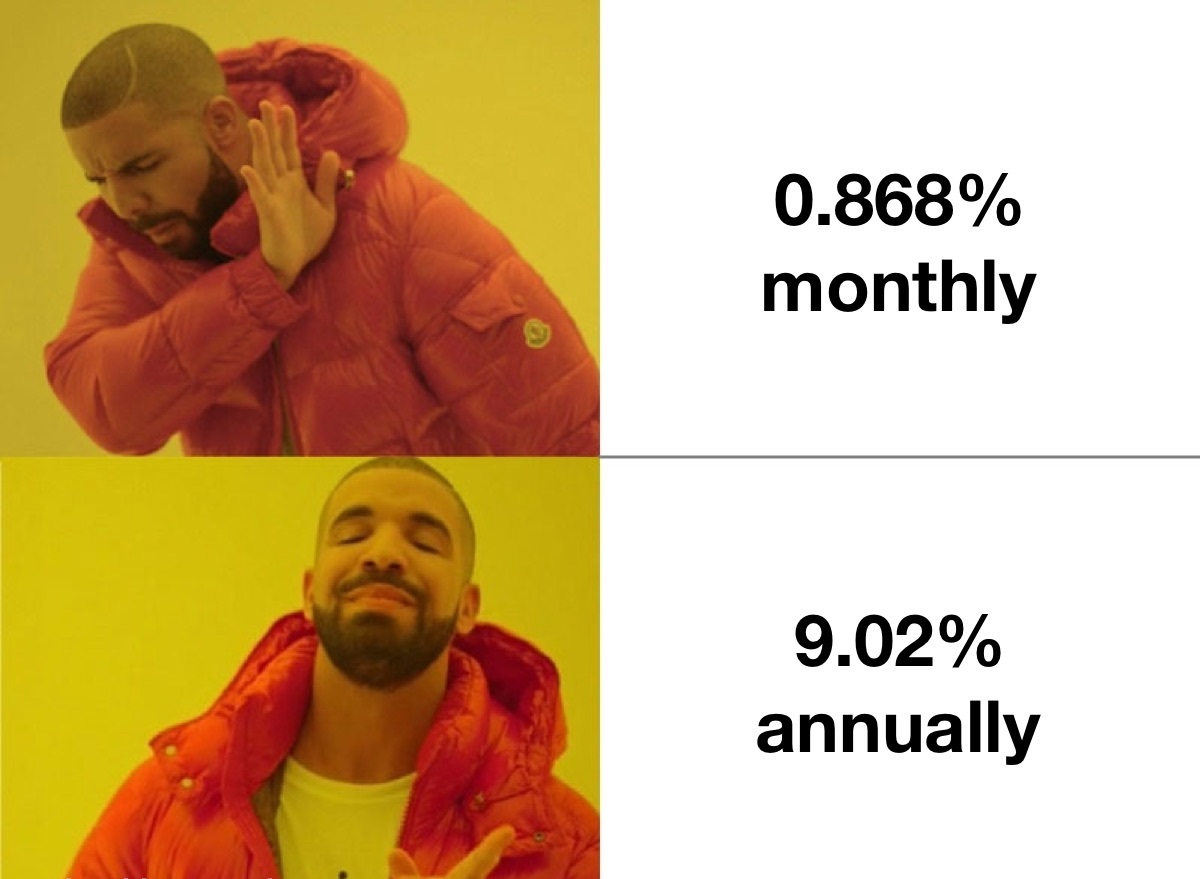

Firstly, what’s the return on the option premium? If you bought 100 shares of VTI today for $161.27, then the option premium alone would be a return of 0.868% (= $140 ÷ $16, 127 × 100%).

Compound It

If you just rolled your eyes and shut your brain off, you need to rethink in terms of yearly compounding. That option expires 35 days from now, and there are 365 days in a year. If you could make 0.868%, and compound it 10 times over the course of a year, you’d have made 9.02% off options premiums alone.

- That’s better than the average long-term total market return of 7%.

- That 9.02% is the return from options premium alone, not accounting for the potential additional profits if VTI happened to appreciate to your strike price.

You can use this method to calculate a theoretical annual return for your options— if you were going to make something in one month, multiply it by 12 (or compound it twelve times assuming reinvestment if you are very optimistic). Look at the number and marvel at how high it is for a yearly return…and then immediately throw the number away, realizing life happens and you rarely actually make that. I have found it to be more of a feel-good number than a realistic goal, which is why it is called a theoretical return. Life happens, stocks move, and it’s rarely that simple.

Not Just Premiums- Returns from Appreciation, Too!

But those returns we just figured didn’t even include potential appreciation! Back to our example— to recap: you’re in it to win it at $16,127 and sold the Jan’ 20 $162 strike call for $140 ($1.40 per share). All the sudden some good news happens— trade deal or blah blah or whatever— and the VTI shoots up to $164 and stays there until expiration.

If you are trading in an IRA and don’t care about capital gains, you could just let the 100 shares of VTI get “called” from you. In that case, you’d be selling them at the strike of the contract— $162

a share. So in addition to the premium you received, you’re making the difference between your purchase price and the strike price, $73 [($162−$161.27)×100 shares]. Add that $73 to your $140 and you’re at $213. $213 is a 1.32% return [($213÷$16127)×100%], better than the premium-only return of 0.868%.

Sounds good— you bought some stuff, and someone paid you money for the right to buy the stuff from you for a higher price than you bought it.

Additionally, the annual return of making 1.32% ten times (it was a 35-day call, not 28 day) is 14%…

A Better ROI Awaits- Selling Calls Against Shares that Already Appreciated

Alternatively, if you got lucky and initially bought those VTI shares on Feb 12th, 2016 when VTI had a dip to $94.36, and have been holding ever since, your $140 premium alone would be getting you a 1.48% return on your investment ($140 ÷ $9436). One neat thing to realize is that if you sell calls on your already-appreciated shares, your premiums will account for a higher % of the original cost. Although this isn’t really amazingly insightful, it would be nice to have a double-bagger1 that could start to pay itself off while you still let the shares ride.

This is all well and good, but you have to keep in mind that if you let those shares get called, you will have to pay taxes on the gains VTI accumulated and the premium you were paid (unless you are trading in an IRA, which I’d recommend at least to start).

LEAP Calls and Their Deceptively High Premiums

This is all well and good, but you have to keep in mind that if you let those shares get called, you will have to pay taxes on the gains VTI accumulated and the premium you were paid (unless you are trading in an IRA, which I’d recommend at least to start).

LEAPS Calls and Their (Deceptively?) High Premiums

Just as a teaser— if you look at the options chain for March, which is 98 days away from when I took the data, the premiums go up a lot. And they increase for all the strikes, even the ones that are way out of the money.

Instead of $140 for a $162 strike, you could get $260 for a $164 strike call— substantially more premium AND more than $200 of potential share appreciation [($161.27 to $164) ×100 shares] before your stock hits the strike price and gets called at expiration.

Time Value Inequality

But before you let that tempting premium entice you into only selling farther-dated calls, take a closer look at the $162 strike for 98 days out. It’s got a bid-ask of $3.70–$3.90, so you’ll probably get $3.80 for it. Compare that to the roughly one month return of $1.40.

There’s an inequality! This 3-month call does not trade for 3 times the value of $1.40 ($4.20), it trades for about 10% less than that. And if you went farther out, that time value inequality would be even starker.

As an exercise to reinforce this time-value inequality, pick any stock with LEAPS (2 year call expiration dates). Then figure out the premium per day you get on the one month call versus the premium per day on the 2 year call…I’d bet dollars to donuts it’s less dollars per day. Just remember, the premium received per day is always less for further dated options contracts.

Now that you understand all that, time to move on to more things to think about when selecting a strike.

Next- Article 16: Strike Selection Part 2

Previous- Article 14: Overwriting and Returns

- A double-bagger is the trading term for a stock that doubled since the time

you bought it, representing a 100% return. [↩]